Why TDS Is a Key Issue for NRIs

Tax Deducted at Source (TDS) is one of the most common—and confusing—tax topics for NRIs with income from India. Whether it’s rent, interest, dividends, or proceeds from selling property, TDS for NRIs is often higher and stricter than for resident Indians.

This difference exists because Indian tax law places the responsibility of tax collection on the payer when the recipient is a non-resident. Understanding how TDS works, which rates apply, and what remedies are available can help NRIs manage cash flow better and avoid unnecessary tax lock-ins.

What Is TDS?

Tax Deducted at Source (TDS) is a mechanism where tax is deducted by the payer at the time of making a payment and deposited with the Indian government on behalf of the recipient.

For NRIs:

- TDS is deducted on most India-sourced income

- Deduction often applies to the gross amount, not just the profit

- Refunds, if any, must be claimed by filing an Indian tax return

Why Is TDS Higher for NRIs?

TDS rates for NRIs are higher because:

- Indian authorities cannot easily enforce tax recovery from non-residents

- The law assumes a conservative approach to ensure tax collection

- Section 195 of the Income Tax Act mandates deduction on payments to non-residents

As a result, even if the actual tax liability is lower, TDS may still be deducted at higher prescribed rates.

Actual rates may vary based on income level, surcharge, and DTAA applicability.

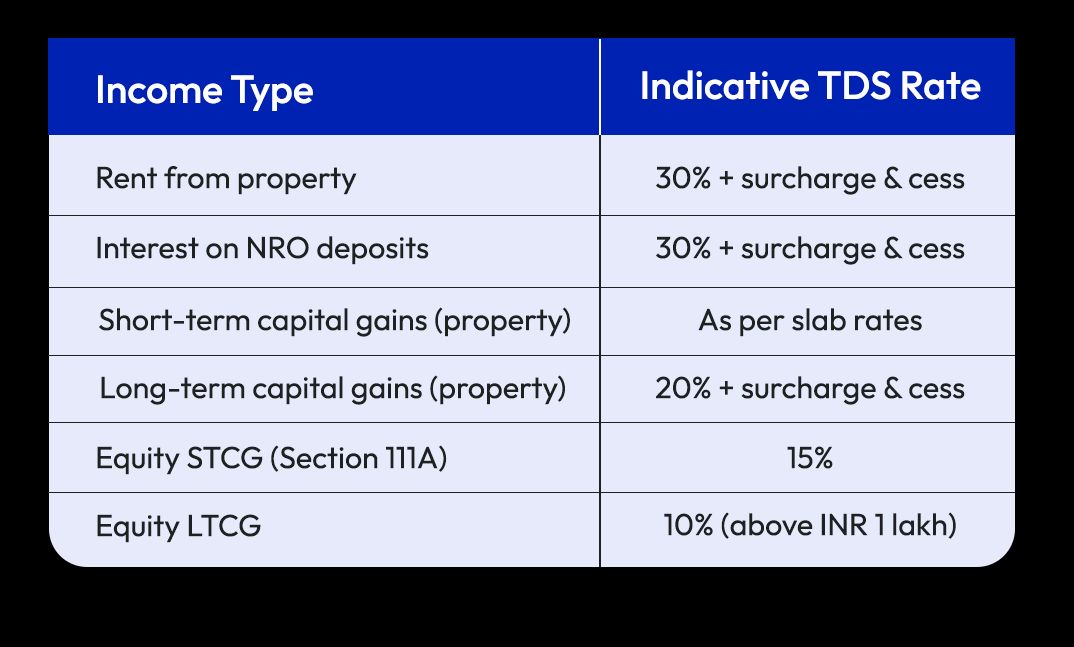

TDS on Sale of Property by NRIs

One of the most significant TDS implications for NRIs arises during property sales.

Key points:

- Buyer is responsible for deducting TDS

- TDS applies on the sale value, not just the gain

- Rate can exceed 20–30% depending on the nature of gains

This often leads to a large amount being blocked until the NRI files a tax return and claims a refund.

How NRIs Can Reduce Excess TDS

Indian tax law provides legitimate ways to reduce or avoid excess TDS.

DTAA Benefits

If India has a Double Taxation Avoidance Agreements (DTAA) with the NRI’s country of residence, lower TDS rates may apply, subject to documentation.

Lower or Nil TDS Certificate (Section 197)

NRIs can apply to the Income Tax Department for a lower or nil TDS certificate if their actual tax liability is lower than the prescribed TDS rate.

Accurate Income Classification

Correctly identifying income type and applicable sections helps prevent incorrect deductions.

Filing Returns and Claiming Refunds

If excess TDS is deducted:

- NRIs must file an income tax return in India

- Refunds are processed after assessment

- Processing timelines may vary

Filing returns is often mandatory for NRIs with Indian income, even if tax has already been deducted.

Common Mistakes NRIs Make

NRIs often face issues due to:

- Not applying for a lower TDS certificate in advance

- Assuming DTAA applies automatically

- Not filing returns to claim refunds

- Misunderstanding buyer or bank responsibilities

Early planning helps avoid cash flow stress.

FAQs: TDS for NRIs

Is TDS mandatory on all NRI income?Most India-sourced income is subject to TDS, but rates vary by income type.

Can NRIs avoid TDS completely?TDS cannot usually be avoided, but it can be reduced through DTAA or lower TDS certificates.

Who deducts TDS on property sales?The buyer is legally responsible for deducting and depositing TDS.

Is filing an Indian tax return mandatory for NRIs?Yes, especially if excess TDS has been deducted or refunds are to be claimed.

Does TDS mean final tax?No. TDS is an advance tax; final liability is determined when filing returns.

Final Thoughts

TDS is one of the most impactful tax mechanisms affecting NRIs with income from India. While higher rates can strain cash flow, understanding the rules, planning ahead, and using available legal remedies can significantly reduce the burden.

For NRIs, proactive tax planning is the key to ensuring that TDS does not become an unnecessary financial obstacle.

Sources & Disclaimer

The information in this article is based on publicly available provider disclosures, marketing materials, industry reports, and general remittance market practices at the time of writing. Exchange rates, fees, transfer speeds, and availability may vary by country, payment method, bank, and time period.

Company names mentioned are included for illustrative and comparative purposes only. Any performance metrics, pricing examples, or user experiences referenced reflect advertised claims or individual reports and should not be treated as guarantees. Readers are encouraged to verify live rates, fees, and terms directly with the service provider before initiating a transfer.

This content is intended for informational purposes only and does not constitute financial advice, investment advice, or a recommendation of any specific service.