Send Money from Netherlands to India in 2026: Fees, Exchange Rates & Best Options

-

Author

Rishi Agarwal -

Date

July 8, 2026 -

Read Time

8 Min

TABLE OF CONTENTS

You check the EUR/INR exchange rate on Google before sending €2,000 to your parents in Pune. Then you check what your bank is actually offering. The gap between those two numbers is often €40–70, money that just quietly disappears, not as a fee you can see, but as a worse exchange rate buried in the transaction. Multiply that by every transfer you make in a year, and it adds up to a real amount of money that never needed to leave your pocket.

Sending money from the Netherlands to India has become genuinely straightforward, but “straightforward” doesn’t mean cheap or fast by default. Whether you’re an NRI supporting family back home, paying for property, or covering education fees, the transfer method you pick can save or cost you a meaningful amount.

This guide covers the most practical, current options for EUR to INR transfers in 2026, with real costs, realistic timelines, and what actually matters when you’re sending regularly.

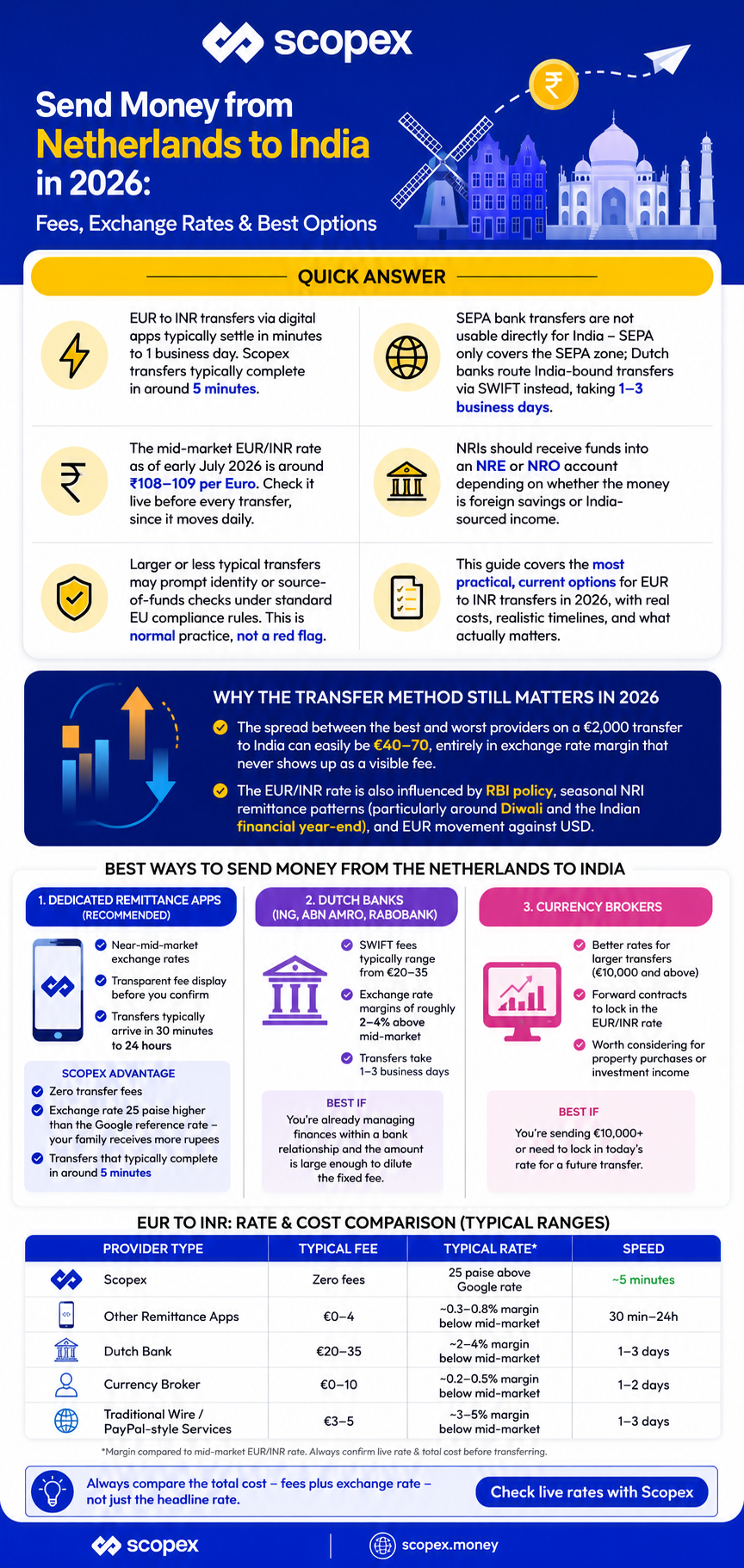

Quick Answer

- EUR to INR transfers via digital apps typically settle in minutes to 1 business day. Scopex transfers typically complete in around 5 minutes

- SEPA bank transfers are not usable directly for India – SEPA only covers the SEPA zone; Dutch banks route India-bound transfers via SWIFT instead, taking 1–3 business days

- The mid-market EUR/INR rate as of early July 2026 is around ₹108-109 per Euro. Check it live before every transfer, since it moves daily

- NRIs should receive funds into an NRE or NRO account depending on whether the money is foreign savings or India-sourced income

- Larger or less typical transfers may prompt identity or source-of-funds checks under standard EU compliance rules. This is normal practice, not a red flag

Why the Transfer Method Still Matters in 2026

Dutch residents have more transfer options than ever; traditional banks, fintech apps, and currency brokers all compete for this corridor. But the spread between the best and worst providers on a €2,000 transfer to India can easily be €40–70, entirely in exchange rate margin that never shows up as a visible fee.

The EUR/INR rate is also influenced by RBI policy, seasonal NRI remittance patterns (particularly around Diwali and the Indian financial year-end), and EUR movement against USD. Keeping an eye on timing, not just the provider, pays off. For a deeper look at what actually moves this specific rate, see our guide on how the EUR to INR rate works.

Best Ways to Send Money from the Netherlands to India

1. Dedicated Remittance Apps (Recommended)

Digital platforms have made EUR-to-INR one of their most competitive corridors. Key advantages:

- Near-mid-market exchange rates

- Transparent fee display before you confirm

- Transfers typically arrive in 30 minutes to 24 hours

- Convenient mobile-first experience

ScopeX, built specifically for the European NRI market, offers:

- Zero transfer fees

- An exchange rate 25 paise higher than the Google reference rate, meaning your family receives more rupees than a straight mid-market conversion would give them

- Transfers that typically complete in around 5 minutes

It’s particularly well-suited for recurring transfers, a common need for anyone supporting family in India regularly. You can check today’s live rate on our Netherlands to India corridor page.

2. Dutch Banks (ING, ABN AMRO, Rabobank)

Established Dutch banks can send international transfers, but the cost profile is different:

- SWIFT fees typically range from €20–35 per transfer

- Exchange rate margins of roughly 2–4% above mid-market are common

- Transfers take 1–3 business days

This works if you’re already managing finances within a bank relationship and the amount is large enough to dilute the fixed fee. For regular, smaller transfers, the cumulative cost adds up fast. Our breakdown of banks vs. money transfer apps goes through the maths in detail.

3. Currency Brokers

For larger transfers generally €10,000 and above, specialist currency brokers can sometimes negotiate better rates than a standard app and offer forward contracts to lock in the EUR/INR rate for future transfers. Worth considering if you’re repatriating investment income or handling a property purchase, where the transfer size justifies the extra setup.

EUR to INR: What Affects the Rate You Get

The mid-market EUR/INR rate as of early July 2026 is trading at approximately ₹108–109 per Euro, though like any currency pair, it moves daily and has ranged between roughly ₹105 and ₹112 over the past several months. What each provider adds on top of that mid-market rate is where the real cost difference lies, not the headline rate itself.

| Provider Type | Typical Fee | Typical Rate | Speed |

| ScopeX | Zero fees | 25 paise above Google rate | ~5 minutes |

| Other Remittance Apps | €0–4 | ~0.3–0.8% margin below mid-market | 30 min–24h |

| Dutch Bank | €20–35 | ~2–4% margin below mid-market | 1–3 days |

| Currency Broker | €0–10 | ~0.2–0.5% margin below mid-market | 1–2 days |

| Traditional Wire / PayPal-style Services | €3–5 | ~3–5% margin below mid-market | 1–3 days |

Figures for “Other Remittance Apps,” “Dutch Bank,” “Currency Broker,” and “Traditional Wire” rows are typical ranges based on general market patterns as of 2026, not quotes from any specific named competitor. Always confirm the live rate and total cost directly with a provider before transferring, since these vary by amount, payment method, and day. ScopeX figures reflect our standard published pricing at the time of writing.

NRE vs NRO Accounts: Where Should the Money Land?

If you’re a Non-Resident Indian sending money home, the receiving account type matters:

- NRE Account (Non-Resident External): Principal and interest are fully repatriable; funds in this account come from foreign earnings. Interest is tax-free in India.

- NRO Account (Non-Resident Ordinary): Used for income earned in India (rent, dividends). Repatriation is allowed up to USD 1 million per financial year, subject to tax compliance.

Most remittance platforms support transfers to both account types. Confirm with your Indian bank which SWIFT/IFSC details to use. If you’re regularly moving money out of an NRO account specifically (for example, rental income or investment proceeds), our NRO account transfer guide covers the documentation and limits in detail, and our repatriation guide covers the broader FEMA framework across NRE, FCNR, and NRO accounts.

If the funds you’re sending relate to selling property or investments in India rather than everyday savings, that’s a separate tax event. See our Capital Gains Tax for NRIs guide before you transfer.

Compliance and Documentation in the Netherlands

Dutch residents sending money abroad are subject to EU anti-money laundering regulations. In practice, this means:

- Regulated providers, banks and licensed remittance platforms alike must verify your identity (KYC) before you can transact, typically as a one-time onboarding step

- For larger or less typical transfers, a provider may request source-of-funds documentation as part of its own risk-based checks — this is standard practice across the industry, not specific to any one platform or to India transfers

- Regular large transfers may prompt a routine review from your provider

A note on specific thresholds: EU anti-money laundering rules are currently mid-transition the existing framework applies today, while a new EU-wide regulation (AMLR) is scheduled to take effect from 10 July 2027 and will change some of the specific figures involved. Because exact thresholds vary by regulation currently in force, by how the Netherlands has implemented it, and by each provider’s own risk policy, we’ve deliberately kept this section general rather than quoting a specific euro figure that could go stale or be wrong for your specific situation. If you need the precise current threshold for a specific transfer, your provider’s compliance team or a Dutch financial advisor can confirm it.

This isn’t a barrier it’s standard practice across every regulated provider, bank or app. Legitimate platforms handle it smoothly with a one-time verification process rather than repeated friction on every transfer. If you’re evaluating a provider you haven’t used before, it’s worth knowing what red flags to check before trusting them with a large amount, and understanding whether a “zero fee” claim is genuinely zero-cost or just restructured into the exchange rate.

FAQ: Sending Money from Netherlands to India

How long does a bank transfer from the Netherlands to India take?

Via SWIFT (used by Dutch banks), transfers to India take 1–3 business days. Digital remittance apps typically deliver within minutes to 24 hours. SEPA cannot be used directly for India transfers, as it only covers the SEPA zone (EU plus a few neighbouring countries).

What is the cheapest way to send euros to India from the Netherlands?

Dedicated remittance platforms typically offer the lowest all-in cost for most transfer sizes, combining low fixed fees with near-mid-market exchange rates. For amounts above roughly €10,000-€15,000, it’s worth comparing a currency broker’s rate as well, since the setup cost of a broker relationship starts to pay off at that size.

Is there a limit on how much I can send to India from the Netherlands?

There’s no fixed legal cap for Dutch residents, but larger or unusual transfers may require source-of-funds documentation as part of standard EU compliance checks, and Indian receiving limits apply depending on the account type. NRO accounts can receive up to USD 1 million annually in repatriation.

Do I need an NRI account to receive money in India?

Not strictly, money can be sent to a regular Indian savings account. However, NRE/NRO accounts offer tax benefits and repatriation flexibility that make them the practical choice for most NRIs. See our safety and provider-selection guide if you’re setting up a transfer for the first time.

Is it safe to send a large amount online instead of using my bank?

Yes, provided you use a regulated provider. Being asked for identity verification or source-of-funds documentation on a large transfer is standard EU compliance practice, not a sign that something is wrong. The providers worth avoiding are the ones that skip this step entirely.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Exchange rates and fees are indicative, fluctuate constantly, and are subject to change always verify current rates directly with your chosen provider before transferring. ScopeX is a registered money service business; regulatory details are available at (https://scopex.money/privacy-policy/).

Rishi is a Chartered Accountant (ICAI) and CFA (USA) currently heading Finance at ScopeX Fintech. With experience spanning fintech operations and strategic financial leadership, he writes sharp, practical insights on fundraising, financial modeling, risk, and more, bridging the gap between theory and the real fintech world.

RELATED ARTICLES

-

Best App to Send Money from Germany to India in 2026

Quick Summary The best app to send money from Germany to India in 2026 combines a near-mid-market exchange rate, low or zero fees, and fast rupee delivery. Scopex stands out on this corridor with zero transfer fees, an exchange rate that is typically 25 paise higher than the Google reference rate (meaning recipients get more […]

-

How to Send Money from Ireland to India Without Hidden Fees

TL;DR Most banks charge 3–5% above the real EUR to INR rate, plus SWIFT fees that eat into every transfer. The cheapest way to send money from Ireland to India is through a specialist remittance platform like Scopex – zero transfer fees, rates within 25 paise of the mid-market rate, and most transfers land in […]

-

Top 10 International Money Transfer Apps to Send Money to India from Europe

Best Money Transfer Apps to Send Money to India from Europe One of the top money transfer apps for sending money to India from Europe in 2026 is ScopeX. It charges zero transfer fees and gives you 25 paise above the Google mid-market rate, meaning your family receives more rupees than the real exchange rate […]