Banks vs Money Transfer Apps: Best Way to Send Money to India

-

Author

Rishi Agarwal -

Date

March 18, 2026 -

Read Time

7 min

TABLE OF CONTENTS

Banks vs Money Transfer Apps: Best Way to Send Money to India

Sending money from Europe to India can cost more than you expect. Traditional banks are reliable, but they charge high fees and take days to process an international transfer. In contrast, modern money transfer apps promise fast, low-cost transfers with transparent rates. This guide compares the two methods; banks and apps, focusing on costs, exchange rates, speed, and convenience. We also look at real exchange rates (around €1 ≈ ₹103.3 in Nov 2025) and tips for getting the best deal when sending euros to India.

Banks: Slow Transfers and Multiple Fees

Banks often use wire transfers (SWIFT) to send money abroad. While secure, these transfers are slow and expensive. A single international wire transfer can cost €20–50 or more in fees, plus a markup on the exchange rate. For example, even if the market rate is €1 = ₹103.3, a bank might use €1 = ₹100 in its calculations. This mark-up spread in exchange rate (roughly 1 – 2% above mid-market) can cost you hundreds of rupees on large transfers.

Moreover, banks may charge separate fees at each step. Correspondent banks in the chain often deduct ₹300–₹1,000 before the money reaches India. The recipient’s bank in India may also apply service charges and taxes on incoming transfers. In practice, this means part of your sent money never reaches India. According to worldbank, you could send ₹50,000 from Europe but receive only around ₹47,000 – ₹48,000 in an Indian Account after all fees and markups.

Banks also take time. A standard wire from Europe to India can take 2–5 business days or more for complete settlement. Delays happen on weekends and holidays, and you get no live updates. In summary, banks charge fixed fees, and use mark-up for exchange rates, and the total cost is often hidden. For many senders, banks usually end up being the most expensive way to transfer money.

Money Transfer Apps: Faster and Cheaper

Money transfer apps are built for international remittances. They use technology to cut costs and speed up transfers. Most apps disclose all fees and rates upfront. They typically charge an up front flat fee (often just a few euros or pounds) and use the real mid-market exchange rate, rather than adding a markup. This means more of your money arrives. Crucially, the transfer cost is known to you in advance.

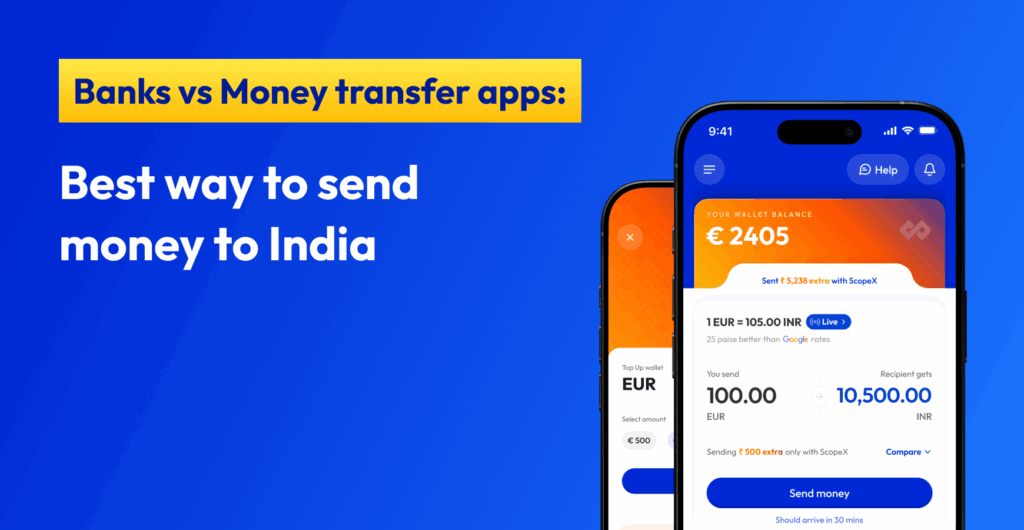

Key advantages of money transfer apps: They usually offer low (or zero) fees, fast delivery, and rate transparency. Many transfers arrive in minutes or hours, even on weekends. Apps also allow real-time tracking so you see when the money reaches the bank in India. Some apps even integrate with India’s UPI system. If you send to an UPI ID, funds can appear instantly in the recipient’s bank account.

Real Exchange Rates

Exchange rates vary daily based on Global Economic Events. For example, mid-November 2025 saw €1 ≈ ₹103. Some apps advertise Google rates or mid-market rates. Aspora, an Indian diaspora app, promises “lightning fast transfers at guaranteed Google rates”. This means they match the rate you see on Google. By using these rates, apps maximize the rupees your recipient gets. In contrast, banks usually subtract 1 – 2% from the mid-market rate as profit.

Real-time rate tools (like Google or xe.com) can give you a benchmark. If an app shows a rate close to that benchmark, it’s giving you a very good deal. For example, if Google says €1 = ₹103.2, and an app offers ₹102.9 or ₹103.0, that is excellent. Always compare the final payout (including both fees and rates) to ensure you get the best EUR to INR rate overall.

Speed and Convenience

Money transfer apps win on speed. Apps work 24/7 on your phone or laptop, no branch visit or paperwork is needed. Once you set up an account and link your bank or card, you can send at any time. Many transfers land within 30 minutes or less. ScopeX, for instance, reports 85% of transfers arrive in under 30 minutes. Some apps offer cash pickups or mobile wallet transfers if the recipient prefers. This flexibility is useful if your family doesn’t have a bank account, for example, you could send cash to a pickup location in India.

Apps also include security features like two-factor authentication and encryption. They are regulated by financial authorities and use the SWIFT network or local banking rails securely. In short, you get bank-level security with much more convenience.

NRIs and Specialized Transfer Apps

Non-Resident Indians (NRIs) have specific needs for sending money home. Over a million NRIs in Europe use apps tailored for Indians. These apps often support multiple European currencies and connect directly to Indian banks or payment systems.

For example, apps like ScopeX, Aspora, and others focus on the Indian market. They advertise features like zero transfer fees and no hidden fees. They also claim “256-bit encryption” and round-the-clock support.

Such apps usually support UPI transfers and a wide network of Indian banks (Axis, HDFC, SBI, ICICI, etc.). If your recipient has a UPI ID, apps like Remitly or Wise (with Indian on-boarding) let you send directly, bypassing bank fees. This makes the transaction even faster and cheaper for common domestic payments.

Example: A Real Transfer Scenario

Imagine Sara, an NRI in Germany, needs to send €500 to her parents’ account in Mumbai. Her bank charges a €15 fee and offers a rate of €1=₹100. This means Sara pays €15 and gets ₹50,000 total at the bank’s rate. Meanwhile, an app charges only €3 and uses €1=₹103. Sara still pays €3, but now her parents get about ₹51,500. That’s ₹1,500 more in their pocket, and the transfer finishes in 20 minutes instead of days. This real-world example shows how low-fee apps deliver more rupees and save time.

Tips for Cheaper Transfers

- Compare providers regularly. Exchange rates and fees change often. Don’t stick to one option by habit. Before each transfer, check a few services.

- Focus on final payout. Ignore headlines like “zero fee” or “low fee” unless you see the exchange rate. The goal is the most INR received. A small fee with a great rate usually wins over no fee with a poor rate.

- Avoid credit cards. Paying with a credit card adds cash-advance fees and worse rates. Use a bank debit or transfer balance instead.

- Send on weekdays. Some weekends or local holidays trigger higher bank markups. Mid-week transfers often give better rates.

- Use transparent apps. Choose apps that show exactly how much the recipient will get (including all fees) before you send.

By following these tips and using modern apps, European senders can ensure they send money to India quickly and keep more for their families.

Which Option is Best?

For most people, money transfer apps are the smarter choice. They beat banks on cost, speed, and convenience. Conversely, large corporations requiring official documentation typically favor traditional banks. One can ask the bank for any fee waivers or special rates.

New fintech platforms are specifically targeting NRIs. For instance, ScopeX (an app built by Indians for Indians) highlights “Zero fees. More rupees.” on transfers from Europe to India. It serves 100+ European banks and 50+ Indian banks, with quick 30-minute transfers. Such services exemplify how the remittance market is changing: old wires give way to digital rails with live tracking and near-market exchange rates.

Sources & Disclaimer

The information in this article is based on publicly available provider disclosures, marketing materials, industry reports, and general remittance market practices at the time of writing. Exchange rates, fees, transfer speeds, and availability may vary by country, payment method, bank, and time period.

Company names mentioned are included for illustrative and comparative purposes only. Any performance metrics, pricing examples, or user experiences referenced reflect advertised claims or individual reports and should not be treated as guarantees. Readers are encouraged to verify live rates, fees, and terms directly with the service provider before initiating a transfer.

This content is intended for informational purposes only and does not constitute financial advice, investment advice, or a recommendation of any specific service.

Rishi is a Chartered Accountant (ICAI) and CFA (USA) currently heading Finance at ScopeX Fintech. With experience spanning fintech operations and strategic financial leadership, he writes sharp, practical insights on fundraising, financial modeling, risk, and more, bridging the gap between theory and the real fintech world.

RELATED ARTICLES

-

What Are Zero-Fee International Transfers & Are They Really Free?

Money-transfer apps often advertise “zero fees” on international transfers, which sounds great for NRIs in Europe sending cash home. In reality, “zero fee” usually means no upfront charge but the provider may still earn through the exchange rate or other costs. For example, some services waive transfer fees but add a hidden markup: they give […]